Maintenance AI and Insurance Risk: 2026 Playbook for PMs

Learn how Maintenance AI and Insurance Risk intersect in property ops: faster leak response, audit-ready logs, and 2026 governance controls. See how.

TL;DR

Maintenance AI refers to always-on AI agents that handle tenant calls, triage emergencies, create work orders, and dispatch vendors, and it directly changes how insurers assess your risk profile. Water damage is the number one loss driver in multifamily housing, and the speed of your response determines whether a small leak becomes a six-figure claim. Operators who pair AI triage with leak detection and proper documentation can demonstrate lower loss severity to underwriters, while those who deploy AI without governance controls introduce new liabilities that carriers are starting to scrutinize.

At a Glance: How Maintenance AI Reduces Insurance Risk

In 2026, Maintenance AI reduces property insurance risk by automating the "First Notice of Loss" (FNOL) and slashing response times for water damage—the #1 driver of multifamily claims. By providing 24/7 triage, instant containment instructions, and time-stamped documentation, AI agents prevent Category 1 water from escalating into high-cost Category 3 losses. Operators using AI-driven maintenance typically see:

- 70% reduction in water claim severity via faster mitigation.

- 10% premium discounts for paired leak detection/auto-shutoff systems.

- Lower litigation risk through auditable, real-time maintenance logs.

What “Maintenance AI” Means in Property Operations

In property management, maintenance AI is an AI agent that answers tenant maintenance calls (voice, SMS, or email), classifies whether the issue is an emergency or routine request, creates work orders directly in your PMS, dispatches vendors from preferred lists, and follows up after work is completed. It replaces or augments the after-hours answering service and handles intake around the clock.

The insurance angle is what makes this term worth defining separately. These AI agents change an owner’s risk profile in two directions simultaneously. On the positive side, they shorten time-to-notice and time-to-mitigation for high-severity losses (especially water), and they generate auditable records that help with claims defense and habitability disputes. On the negative side, they introduce AI governance duties that insurers and regulators now expect you to manage.

That dual nature, reducing traditional property risk while creating new technology risk, is what “maintenance AI and insurance risk” actually describes.

For a deeper look at how AI agents function as maintenance coordinators beyond simple chatbots, see this guide to AI maintenance coordinators in property management.

Why Insurers Care: Water Is the Number One Loss in Multifamily

Before getting into how maintenance AI changes outcomes, it helps to understand why underwriters pay attention to maintenance operations at all.

Water damage is the leading cause of loss in apartment properties. The National Multifamily Housing Council (NMHC) explicitly advises operators to invest in leak detection and preventative maintenance as core strategies for improving insurance outcomes at renewal (NMHC, 2023 State of Multifamily Risk). This isn’t a peripheral recommendation. It’s central to their risk guidance.

The trend data reinforces the urgency. LexisNexis reports that non-weather water claim frequency actually fell in 2024, but severity rose (LexisNexis, 2025 Home Trends Report). Fewer events, but each one costs more. That pattern rewards operators who can catch problems early and respond fast, the exact scenario where maintenance AI and insurance risk intersect most directly.

Table: The Impact of Response Time on Loss Severity

Response Window | Water Category | Typical Mitigation Cost | Insurance Risk Level |

0–2 Hours | Category 1 (Clean) | $2,500 – $5,000 | Low (Contained) |

2–24 Hours | Category 2 (Gray) | $10,000 – $25,000 | Medium (Seepage) |

24–48+ Hours | Category 3 (Black/Mold) | $50,000+ | High (Structural/Health) |

The Clock Starts Immediately

Under IICRC S500 restoration standards, clean Category 1 water (a supply line break, for instance) commonly degrades to Category 2 within roughly 24 to 48 hours if not addressed (IICRC S500 timing reference). Category 2 water requires more aggressive remediation, costs more, and carries higher health risk.

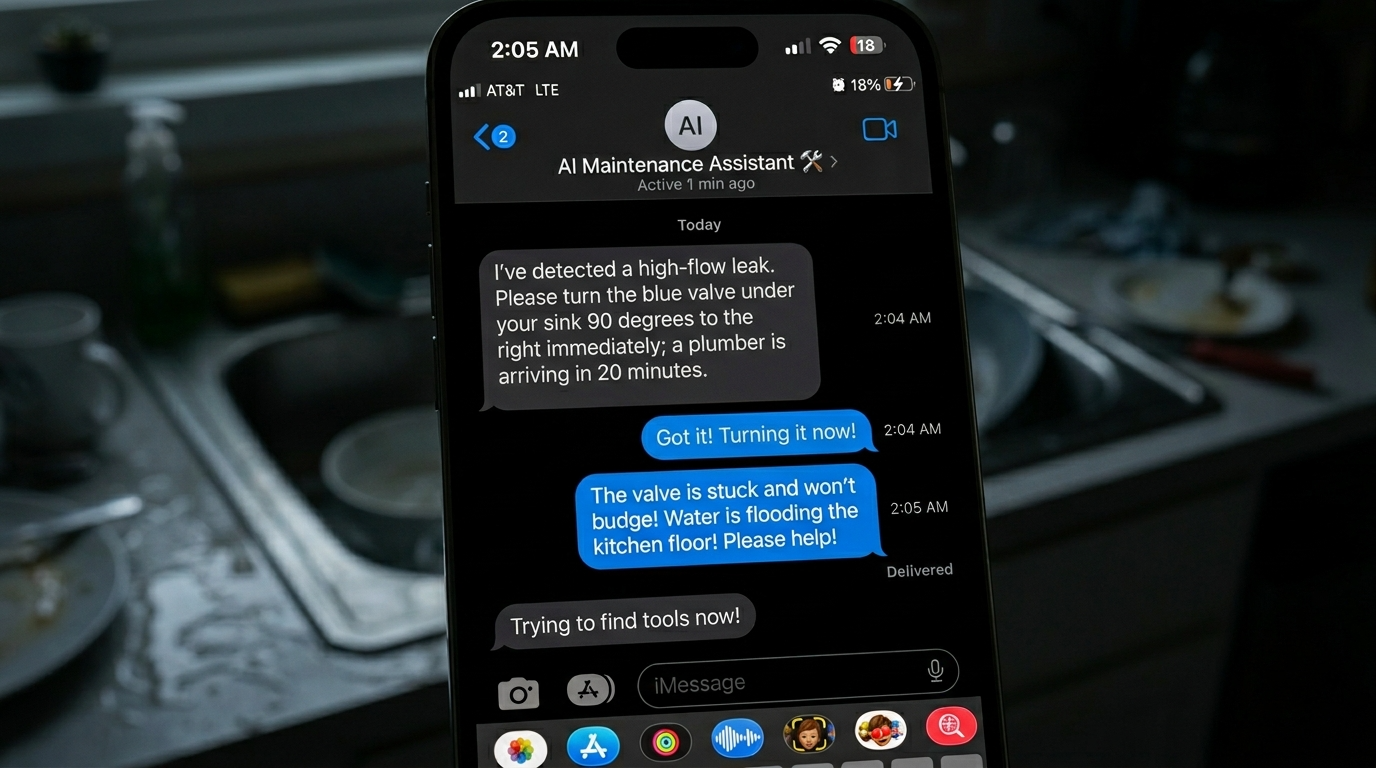

This is the core mechanism. A tenant calls at 2:00 AM about water pooling under the kitchen sink. If nobody picks up and the voicemail sits until 10:00 AM, that’s eight hours of uncontrolled flow. The water may have already degraded. The remediation scope expands. The claim gets bigger.

Restoration professionals in industry forums confirm this. Practitioners on the National Restoration Authority’s platform emphasize that misclassifying an active loss as “non-emergency” during after-hours intake is one of the most common ways scope and insurer disputes expand (National Restoration Authority).

How Maintenance AI Reduces Insurance Risk

The connection between maintenance AI and insurance risk reduction runs through three channels: faster response, better documentation, and compatibility with carrier loss-prevention programs.

After-Hours Emergency Detection

Most severe maintenance losses happen when nobody is available to take the call. A pipe bursts at midnight. A water heater fails on a Saturday. The tenant leaves a message and goes to bed. By morning, the damage has spread across multiple units.

AI agents answer in seconds, around the clock. They classify the issue based on the tenant’s description (active water leak vs. a dripping faucet, for example), advise the tenant on immediate containment steps like shutting off the water supply valve, and dispatch an emergency vendor if needed. That alone can cut hours of uncontrolled water flow.

For operators evaluating how after-hours AI maintenance handling works in practice, the insurance case is straightforward: every hour you shave off the response window reduces the chance of category escalation, mold growth, and multi-unit damage.

Practitioners on Reddit’s r/HomeInsurance confirm this from the claims side. One homeowner described a six-figure water loss and months of displacement that a simple water sensor alert could have prevented. Several insurance professionals in the same thread noted that having temperature, flow, and leak alert logs makes a material difference when substantiating claims with adjusters (Reddit, r/HomeInsurance).

Automatic Documentation and Audit Trails

Insurance adjusters and habitability defense attorneys care about timelines. When did the tenant report the issue? When was the first containment step taken? When was the vendor dispatched? When did they arrive?

Maintenance AI generates these records automatically. Every call or text creates a time-stamped intake record, a PMS work order (in systems like AppFolio or Yardi), a dispatch log, and a record of tenant communications. There’s no gap between a verbal report and a written ticket because the AI creates the work order in real time.

This matters for claims. Restoration industry standards note that response time documentation directly influences how insurers classify contamination categories and scope of work. If you can show the vendor was dispatched within 15 minutes and arrived within two hours, you’re in a different negotiating position than if the first documented response was the next business day.

For a full breakdown of what AI-driven maintenance workflows look like step by step, including how documentation flows into the PMS, that guide covers the operational detail.

Pairing AI Triage With Leak Detection and Auto Shutoff

Carriers are already rewarding sensor-based prevention programs. Chubb offers guidance on point-of-leak sensor placement with potential policy discounts (Chubb water coverage resources). Universal Property & Casualty (UPC) provides an explicit 10% non-hurricane premium discount for properties with automatic water shutoff valves. The OECD has documented a broader trend of insurer-supported sensor programs across multiple markets (OECD, 2023).

The evidence on effectiveness is striking. A LexisNexis study found that leak detection devices reduced water-related claim severity by approximately 70% (Digital Insurance / LexisNexis). That’s directional, not a guarantee, but it shows the scale of impact that detection plus fast response can achieve.

Maintenance AI completes the loop. Sensors detect the problem. The AI receives the alert (or the tenant’s call), confirms the severity, advises containment, and dispatches the vendor. Without that middle step, a sensor alert at 3:00 AM might just be a notification that nobody acts on until morning. With AI triage, the response chain stays intact 24/7.

For operators evaluating the full ROI case for maintenance AI, insurance loss reduction is one of the less obvious but most significant financial benefits.

Habitability and Litigation Risk: Where Slow Maintenance Becomes a Lawsuit

Insurance risk from maintenance failures isn’t limited to property damage claims. Habitability lawsuits are a growing exposure for apartment owners, and they frequently trace back to slow or poorly documented maintenance responses.

Brokers specializing in habitational insurance warn that these claims can trigger multiple policy periods and carry heavy defense costs. CRC Group, a wholesale brokerage, has noted that habitability lawsuits raise new and significant risks for apartment owners and their insurers, particularly when water intrusion leads to mold and the operator’s response timeline is questionable (CRC Group).

The pattern is predictable. A tenant reports a leak. The response is slow (especially after hours or over a weekend). Moisture sits. Mold develops. The tenant withholds rent or files a complaint. The operator tries to evict. The tenant counters with a habitability claim backed by photos of mold growth and a timeline showing delayed response.

Practitioners on Reddit’s r/Landlord discuss these scenarios regularly. In one thread, a landlord who served an eviction notice found themselves facing a habitability counterclaim rooted in delayed water intrusion remediation. Commenters stressed the importance of immediate shutoff steps and documented responses, noting that slow after-hours handling is exactly what creates legal and insurance exposure (Reddit, r/Landlord).

Local regulations make this even more urgent in some markets. In New York City, heat and hot water emergencies trigger 24-hour response expectations, and the city’s Emergency Repair Program can intervene directly if landlords fail to act (NYC HPD). A missed after-hours call about no heat in January isn’t just a maintenance failure. It’s a regulatory violation.

The connection between maintenance AI and insurance risk is clear here. AI agents that answer every call, document the tenant’s exact words, provide containment guidance, and dispatch vendors immediately create the timeline that your attorney and your insurer need. For more on how AI handles emergency maintenance triage and escalation ladders, that guide walks through the decision framework.

What to Show Your Broker and Underwriter

Reducing losses matters, but only if your underwriter knows about it. Most property operators leave premium savings on the table because they don’t present operational improvements in a format underwriters can evaluate.

Here’s a checklist for your next renewal conversation. Bring these items to your broker:

24/7 Coverage Proof

Call-handling dashboards showing coverage hours (all 168 hours per week, not just business hours)

Abandoned-call rate (should be near zero with AI intake)

Average ring-to-answer time

First-Notice-of-Loss (FNOL) Metrics

Ring-to-triage time (how fast the issue is classified)

Ring-to-dispatch time (how fast a vendor is contacted)

Proof of safe shutoff or containment instructions given to the tenant, with timestamps

IICRC-Aligned Standard Operating Procedures

“First 48 hours” SOPs for water losses

Vendor SLAs (response time commitments)

Proof of dehumidification and drying logs when applicable

Contractor hand-off documentation referencing IICRC S500 standards

Leak Sensor Coverage Map

Device locations: water heaters, laundry rooms, mechanical rooms, under sinks in common areas

Any automatic shutoff valves installed

Sample alerts showing the detection-to-response chain

Carriers like Chubb and Amica publish acceptable device lists; bring those specifications to renewal

Loss Run Comparison

12-month loss runs before and after AI deployment

Near-miss register: events that were contained without becoming a claim (these demonstrate prevention value)

Tenant Communication Logs

Time-stamped notices, courtesy alerts, and follow-up messages

Evidence of post-work follow-up communications showing the issue was resolved

This package tells a story underwriters can act on. It shows you’ve moved from reactive maintenance to a documented, time-stamped prevention and response system.

The “First 48 Hours” Maintenance Playbook

For water emergencies specifically, here’s the playbook that aligns with restoration standards and gives you the documentation trail insurers want:

Immediate (0 to 15 minutes):

AI intake classifies the issue as an emergency based on tenant description

Tenant receives safe shutoff or containment instructions (main water shutoff location, breaker reset if safe)

Emergency vendor dispatch initiated from preferred vendor list

Short-term (15 minutes to 2 hours):

Vendor confirms acceptance and estimated arrival

Timed escalation if vendor doesn’t confirm within SLA window

PMS work order created with tenant’s exact description, AI classification, and all timestamps

First 24 hours:

Vendor onsite, moisture readings taken, photos and video documented

Category classification (1, 2, or 3) recorded per IICRC S500

Drying equipment placed if needed; dehumidification logs started

Tenant follow-up confirming status and next steps

24 to 48 hours:

Follow-up moisture readings to confirm drying progress

Scope documentation for insurance (before/after photos, readings, timeline)

Tenant communication logged with updates

This playbook exists at the intersection of maintenance AI and insurance risk management. The AI handles intake, classification, dispatch, and follow-up communication. The vendor handles physical remediation. The PMS captures everything.

What to Log in Every PMS Ticket

For each maintenance event, your work order should capture:

The tenant’s exact words describing the problem (AI transcription)

Time the AI advised shutoff or containment steps

Dispatch acceptance time (when the vendor confirmed)

Vendor onsite arrival time

Photos and video of the condition on arrival

Moisture and temperature readings (for water events)

Tenant follow-up message with timestamp confirming resolution or next steps

This micro-checklist turns routine maintenance into claims-ready documentation. When an adjuster reviews the file six months later, the timeline speaks for itself.

Proactive AI Governance for Insurance Compliance

Underwriters in 2026 are moving beyond "Do you use AI?" to "How do you govern it?" To stay insurable and maintain low-risk status, PMs should adopt the NIST AI Risk Management Framework (AI RMF) structure:

Govern: Define who is accountable for AI maintenance decisions.

Map: Document where the AI interacts with tenant data and emergency dispatch.

Measure: Track AI triage accuracy (e.g., % of emergencies correctly identified).

Manage: Maintain "human-in-the-loop" protocols for high-risk escalations.

New Risks That AI Introduces, and How to Stay Insurable

Maintenance AI and insurance risk isn’t a one-way street. AI reduces traditional property losses, but it creates new exposures that insurers are beginning to evaluate.

Mis-Triage and Operational Error

If an AI agent downgrades an active emergency to a routine request, the delayed response could worsen the loss or create injury exposure. A burst pipe classified as “dripping faucet” sits unaddressed for hours. The resulting damage is worse, and the operator now has a record showing the AI made the wrong call.

The mitigation: human-in-the-loop protocols for edge cases, documented escalation rules, and regular review of AI classification decisions. Log the AI’s reasoning, not just its output.

Privacy and Consent

Call recording and SMS-based troubleshooting must comply with state two-party consent laws where applicable. Privacy practices around AI logging and conversation analytics matter to cyber and E&O underwriters. IAPP reporting shows insurers are already probing basic governance questions when underwriting AI-assisted operations (IAPP).

Regulatory Expectations

The NAIC’s 2023 Model Bulletin establishes expectations for how insurers govern AI systems, and those expectations cascade to the organizations insurers cover (NAIC Model Bulletin). The NIST AI Risk Management Framework (AI RMF) provides a practical structure, organized around four functions: Govern, Map, Measure, and Manage, that operators can reference when asked about their AI controls (NIST AI RMF).

For operators who want to signal maturity, ISO/IEC 42001 (AI management systems) is the emerging process-level standard.

Coverage Gaps

Today’s insurance policies split AI-related incidents across commercial general liability (CGL), cyber liability, and errors and omissions (E&O). Coverage gaps exist between these policies. Brookings has framed where insurance can and cannot absorb AI risks (Brookings), and the practical takeaway is this: ask your broker to map specific AI scenarios (mis-triage leading to property damage, data breach from conversation logs, tenant injury from bad advice) to your current policies and identify gaps.

If you have questions about how Haven handles audit logs, human-in-the-loop configurations, and governance documentation, reach out to the team directly.

How Maintenance AI Works in Practice

Haven’s Maintenance AI is built specifically for property management operations. Here’s what it does:

24/7 maintenance request intake across voice, SMS, and email

Emergency detection and triage that classifies severity and triggers appropriate response protocols

PMS work order creation and updates directly in systems like AppFolio and Yardi

Vendor dispatch from your preferred vendor lists, following your rules

Post-work follow-ups with tenants to confirm resolution

Multi-language voice agents with conversation memory and continuity

These capabilities map directly to what underwriters evaluate: always-on coverage, fast classification, documented timelines, and consistent follow-through.

Explore Haven’s Maintenance AI to see how these workflows translate to your portfolio, or book a demo to see the triage, logging, and dispatch workflows your broker will want to review at renewal.

Frequently Asked Questions

Does maintenance AI actually lower insurance premiums?

It can, but not through a single mechanism. Maintenance AI reduces loss frequency and severity (especially for water damage), which underwriters value when setting rates. Some carriers already discount for leak detection sensors and auto shutoff valves. Bringing AI-generated response logs, loss-run comparisons, and sensor coverage maps to renewal gives your broker concrete evidence to negotiate with. No vendor can promise a specific premium reduction, but lower claims activity and better documentation improve your position.

What metrics should we track for insurance purposes?

Focus on ring-to-triage time, ring-to-dispatch time, vendor arrival time, and evidence of shutoff or containment steps taken before the vendor arrived. Photo and video documentation, moisture readings, and time-stamped tenant communications round out the picture. Adjusters and underwriters look for proof that you acted quickly and documented everything (National Restoration Authority).

What standards should we reference when talking to insurers about maintenance AI?

Three standards matter most. IICRC S500 governs water damage restoration timelines and category classifications. The NAIC Model Bulletin (2023) sets expectations for AI governance in insurance contexts. The NIST AI Risk Management Framework provides the vocabulary (Govern, Map, Measure, Manage) for describing your AI oversight practices. Referencing these shows underwriters you’re operating within recognized frameworks.

Does AI triage create liability if it misclassifies an emergency?

Yes, this is a real risk. If an AI agent classifies a burst pipe as routine and the delayed response worsens the damage, the operator could face increased claim costs or even liability for the classification error. The mitigation is clear escalation rules, human-in-the-loop review for ambiguous cases, and logged decision rationale. Treating AI triage as a tool that assists (not replaces) human judgment on edge cases keeps the risk manageable.

How do leak sensors and maintenance AI work together for insurance purposes?

Sensors detect the problem. AI handles what happens next. A leak sensor alerts at 3:00 AM. The AI agent receives the alert or the tenant’s call, confirms severity, walks the tenant through shutoff steps, and dispatches an emergency vendor. Carriers like Chubb offer potential discounts for sensor programs, and UPC provides a 10% non-hurricane premium discount for auto shutoff valves (Chubb). Pairing both technologies checks two boxes for underwriters: prevention and rapid response.

Where do AI-related incidents fall in current insurance policies?

There’s no single “AI policy” today. Incidents typically split across CGL (if AI advice leads to property damage or injury), cyber liability (if conversation data is breached), and E&O (if AI-driven decisions constitute a professional service failure). Coverage gaps between these policies are common. The best step is to ask your broker to map three to five specific AI scenarios against your current program and identify where you’re exposed.

What’s the most important thing to bring to an insurance renewal if we’re using maintenance AI?

A before-and-after loss run comparison paired with your response-time metrics. Show the underwriter that since deploying AI triage, your average time-to-dispatch dropped, your near-miss count went up (events contained without claims), and your overall loss severity declined. Supplement with your leak sensor coverage map and a one-page summary of your AI governance practices. That package tells the story in language underwriters already use.